Reversionary beneficiaries often hear they have 12 months to “sort things out” after inheriting a pension. Technically, this is true for Transfer Balance Cap purposes — but it may not protect contribution opportunities tied to Total Super Balance.

Example:

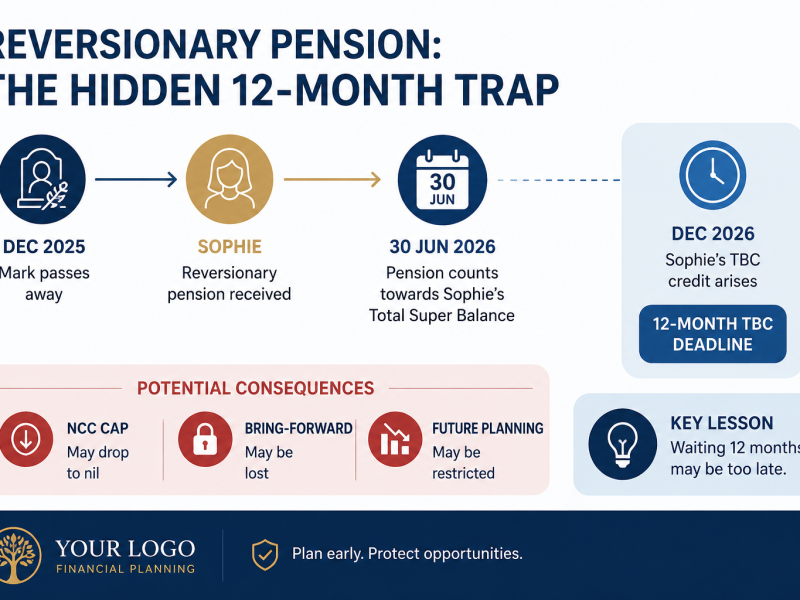

In Mark and Sophie’s case on pages 1–2:

- Mark dies December 2025

- Sophie’s TBC credit delayed until December 2026

- But Mark’s reversionary pension counts toward Sophie’s TSB at 30 June 2026

Potential Consequence:

If Sophie’s TSB exceeds key thresholds by 30 June:

- NCC cap may drop to nil

- Bring-forward may be lost

- Future contribution planning may be significantly reduced

Strategic Lesson:

Waiting until the 12-month TBC deadline may be too late for some planning opportunities.

Contact Us

If you have inherited, or expect to inherit, a superannuation pension, timing can be critical. Contact us here to review your situation and help ensure valuable contribution opportunities are not lost due to unexpected Total Super Balance consequences.

Disclaimer and Warning

The information above is of a general nature only. It should not be used as a source to make financial decisions. It’s also important to note that the legislation and figures related to this topic tend to change regularly and therefore the information above may not reflect the current status. We recommend that if you are looking for advice on this matter, you should contact us.